Conservative segment in euros (Segment B)

Annual subscription deadline: 30th November

Report on the conservative segment

Created in late 2004, the conservative segment invests essentially in bonds and fixed-revenue instruments, to offer an alternative to beneficiaries who wish to protect part or all of their assets against market volatility during their last two years of affiliation. Beneficiaries aged 55 and over can invest in this segment on a voluntary basis, with subscriptions open once a year (at the end of the calendar year for the following year). Beneficiaries decide each year whether they want to invest in the conservative segment, and if so, how much. It is important to understand that the subscriptions are irrevocable, since once the investments are transferred to the conservative segment, they cannot be returned to the traditional growth segment. The reasoning behind this is to protect the beneficiaries against the speculative risks entailed in frequent changes in investment strategy based on market fluctuations.

The conservative segment has preserved asset value since it was created, and even generated a very small profit. This observation highlights the need to have a long-term horizon of at least five years in order to remain fully invested in the growth segment.

When the conservative segment was launched, the Management Board advised beneficiaries to switch their assets over gradually, whenever their time-frame allowed, to dilute the risk of bad timing.

Of course, the final result of this type of transaction obviously depends on market performance over the period. With rhis suggestion we simply wanted to show the potential advantages of carefully planned, gradual transfers.

It is also important to point out that the choice between the growth segment and the conservative segment should not be based on short-term market trends, but rather on each beneficiary’s individual circumstances and ability to tolerate financial risk as well as his/her investment time horizon.

CPIC’s growth segment – the main segment – focuses on generating a return over the long term. It enables you to participate in economic growth through diversified investments, chiefly in stocks and bonds. Its expectation of a higher return is, however, accompanied by short-term volatility which can at times be significant, both upwards and downwards.

In contrast, the conservative segment, which is invested solely in bonds and fixed-income instruments, aims at preserving your assets by considerably limiting volatility, but with the expectation of a lower return

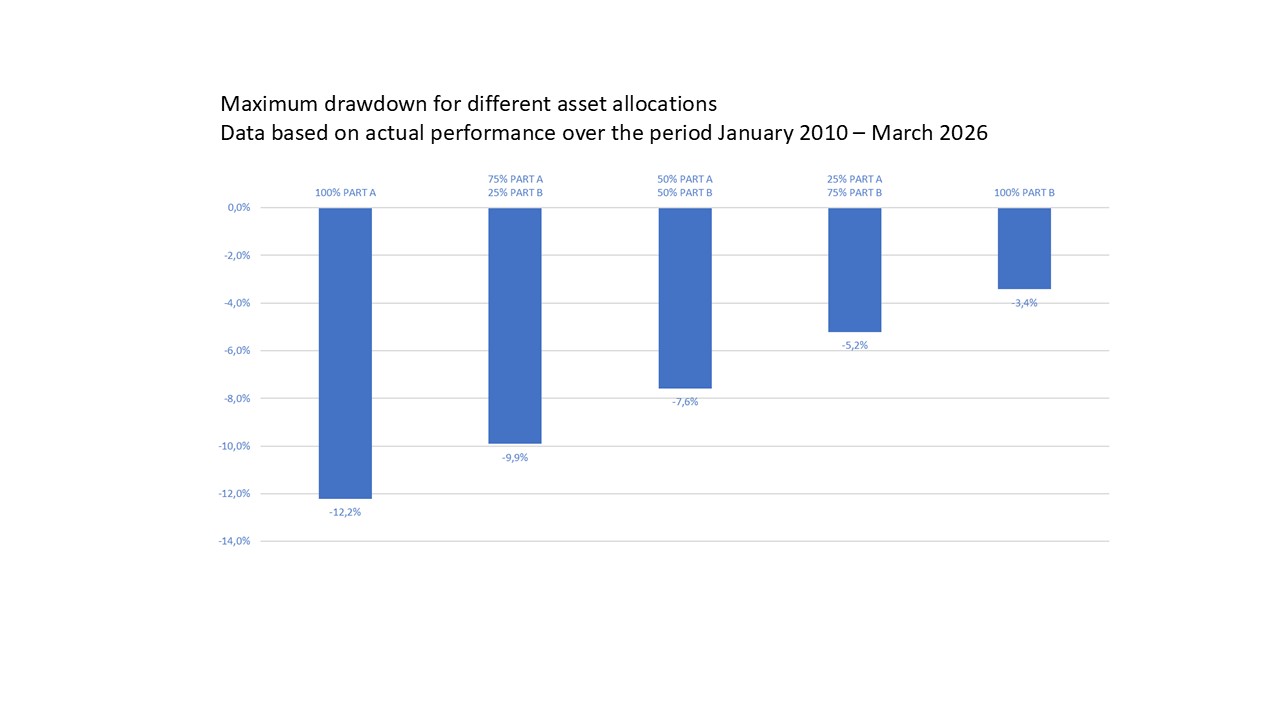

In the present case, gradual transfer to the conservative segment would have reduced the maximum loss.

Simulation of performance is based solely on CPIC’s actual results from January 2010 to March 2026 and, therefore,

does not in any way predict future performance.

Plan your retirement

You are 55 years old or older … You would like to plan your retirement whilst preserving your assets:

The Conference Interpreters’ Provident Fund (CPIC) offers you a solution:

in a conservative segment in euros (Segment B) geared toward approaching retirement.

The growth segment in euros (Segment A), CPIC’s main segment in which your assets are invested, focuses on generating a return over the long term. It enables you to participate in economic growth through diversified investments, chiefly in stocks and bonds. Its expectation of a higher return is, however, accompanied by occasionally high short-term volatility, both upward and downward.

The conservative segment in euros (Segment B), invested solely in bonds and other fixed-income instruments, aims at a reasonable degree of capital preservation by substantially limiting volatility, the price you pay being a lower expected return.

If you are interested, having read the Segment B’s guidelines, please complete the subscription form and return it to the CPIC Secretariat within the indicated time limit.

For detailed figures, please consult the tab “Performance“.